Take Action Now to Reduce Your 2024 Tax Liability

Tax Tips From Cover & Rossiter

We are getting into the busy part of the 1040 tax filing season and even though you’re focused on getting your 2023 tax return filed, now is as good a time as any to start taking steps to reduce your 2024 tax liability. Below are a few changes you can make now that can have a positive impact on reducing your tax burden for this year.

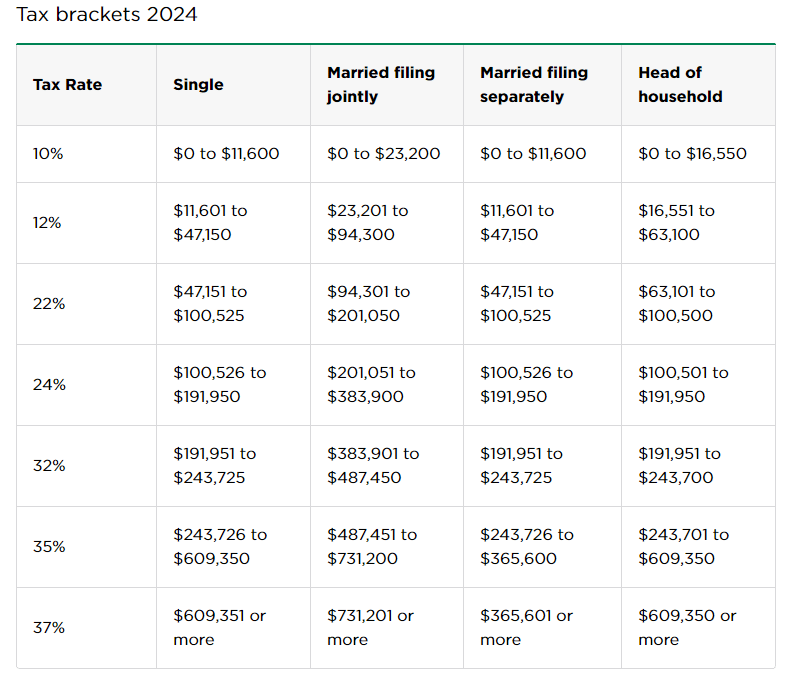

Income tax brackets for 2024

The tax rates themselves didn’t change from 2023 to 2024. There are still seven tax rates in effect for the 2023 tax year: 10%, 12%, 22%, 24%, 32%, 35% and 37%. However, as they are every year, the 2024 tax brackets were adjusted to account for inflation. This year’s increase was 5.4% versus 7% in 2023. That means you could wind up in a different tax bracket when you file your 2024 federal income tax return than the bracket you were in before – which means you could pay a different tax rate on some of your income.

How to get into a lower tax bracket and pay a lower rate

The key, of course, is reducing your taxable income. Fortunately, there are a number of easy (and smart!) things you can do yourself to knock down the taxable income on your next return. For example, putting money into a traditional IRA or 401(k) account will reduce your taxable income because contributions to these accounts are made on a “pre-tax” basis, which means what you put in doesn’t count as income (up to a certain limit). Plus, you receive the added benefit of building your nest egg for retirement.

And, don’t forget about tax credits. While they don’t reduce taxable income because they’re subtracted after your tax is calculated, these are actually more valuable than tax deductions, since they are subtracted on a dollar-for-dollar basis from your tax bill. For example, if you’re in the 22% tax bracket, a $1,000 tax deduction will save you $220 ($1,000 x .22 = $220). However, a $1,000 tax credit can actually be worth $1,000 (unless it’s a nonrefundable credit and your tax bill is less than $1,000). There’s a wide variety of tax credits available, such as for education expenses, saving for retirement, energy-efficient upgrades to your home, buying an electric vehicle or EV charging equipment, having a child, and child and dependent care expenses – just to name a few.

Max out your retirement contributions

As stated previously, less taxable income means less tax owed. Making contributions to a retirement account is a great way to reduce taxable income. There are several options to choose from:

- Company-sponsored 401(k) plans offer a significant benefit because employers often match contributions. Try increasing your 401(k) contribution so that you are investing the maximum amount of money allowed. The maximum contribution limit for 2024 is $23,000, plus an extra $7,500 if you are age 50 or over. If you can’t afford that much, try to contribute at least the amount that will be matched by your employer. Another suggestion would be to increase your annual contributions every time you receive a raise.

- If you don’t have access to a company 401(k), consider contributing to an IRA. For 2024, you can contribute a maximum of $7,000 to an IRA, plus an extra $1,000 if you are age 50 or older.

- If you’re self-employed, consider investing in a Simplified Employee Pension (SEP). You can contribute as much as 25% of your net earnings from self-employment, up to $69,000.

Contribute to a Health Savings Account (HSA)

If you have a high-deductible health care plan, you can reduce your taxable income by contributing to an HSA. A health savings account allows you to make tax-deductible contributions, earn tax-free interest, and withdraw tax-free funds for eligible medical expenses. The 2024 contribution limits are $4,150 for individual coverage and $8,300 for family coverage. Account owners age 55 or older can make an additional $1,000 contribution annually.

Consider a Qualified Charitable Distribution (QCD)

A QCD is a tax benefit that allows owners of individual retirement accounts to transfer funds from their pre-tax IRA directly to qualifying charities. The donated funds count toward satisfying the annual required minimum distribution but are excluded from income, thereby reducing adjusted gross income. In 2024, individuals who are 70 1/2 years old or older may us a QCS to donate up to $105,000 to qualified charities direct from an IRA.

Summary

There are countless tax-saving strategies you can implement at the beginning of the year that can save you from drowning with tax liabilities. Make sure you consult with your trusted advisors, e.g. accountant, financial advisor, attorney, etc., early and often to ensure you are achieving your financial goals while minimizing your tax burden.