Cover & Rossiter Receives Coveted Marvin S. Gilman Superstars in Business Award

Cover & Rossiter is excited to announce they have been awarded The Marvin S. Gilman Superstars in Business Award presented by the Delaware State Chamber of Commerce. The award honors businesses and nonprofit organizations for their achievements and model approaches to business and management.

We are pleased to welcome our newest employees to Cover & Rossiter! Let’s find out a little about them…

Ritika Bothra, Senior Accountant, Audit Department

- Joined Cover & Rossiter: September, 2023

- Prior experience: Worked four years in auditing and assurance at Deloitte USI.

- Education: Bachelor’s in Finance from St. Xaviers College, Kolkata India

- Professional Credentials: CPA: Chartered Accountant, ICAI, India.

- Life outside of work: I love traveling and trying new vegetarian cuisines.

- Favorite quote: “Falling down is not failure. Failure comes when you stay where you have fallen.” – Socrates

==============================================

Chassity Gray, Controller

- Joined Cover & Rossiter: May, 2023

- Prior experience: I worked at BPG Real Estate Services for 14 years in various roles, including accounts payable specialist, accounts payable supervisor, property accountant, development controller, and property controller.

- Education: Bachelor’s degree in Accounting from Strayer University.

- Life outside of work: I enjoy spending time with my husband and two sons. We love taking vacations, going to concerts and spending time with family.

- Favorite quote: “I have not failed. I’ve just found 10,000 ways that won’t work.” – Thomas Edison

==============================================

Marquise Hatcher, Staff Accountant, Tax Department

- Joined Cover & Rossiter: December, 2023

- Prior experience: I spent six years at The Buccini Pollin Group, most recently as a property accountant.

- Education: Bachelor’s degree in Accounting from Goldey-Beacom College, Wilmington DE.

- Life outside of work: I enjoy spending time with friends and family, taking trips to the beach, and traveling the world. I also love to cook healthy meals and work out.

- Favorite quote: “Life is your own marathon. Never stop moving!”

================================================

Paris Hickman, Staff Accountant, Audit Department

- Joined Cover & Rossiter: November, 2023

- Prior experience: Internship at CPA firm, Summer 2023

- Education: Bachelor’s degree in Accounting from Goldey-Beacom College, Wilmington DE.

- Life outside of work: I love to spend time with my family and going on bike rides. I also enjoy working out.

- Favorite quote: “You miss 100% of the shots you don’t take.” – Michael Jordan

================================================

Charles Hunt, Staff Accountant, Tax Department

- Joined Cover & Rossiter: June, 2023

- Prior experience: While in school, I worked as a tax preparer and virtual site coordinator for VITA, a nationwide organization providing tax preparation services to under-privileged communities. I also worked two summer internships in tax accounting and bookkeeping services.

- Education: Bachelor’s degree in Financial Economics from University of Maryland, Baltimore County.

- Life outside of work: I enjoy chess, reading the scriptures, watching and/or participating in all types of sports and competitions, and watching anime.

- Favorite quote: “Let us hear the conclusion of the whole matter: Fear God, and keep his commandments: for this is the whole duty of man.” – Ecclesiastes 12:13

================================================

Jazlee Rojas, Staff Accountant, Tax Department

- Joined Cover & Rossiter: December, 2023

- Prior experience: I worked at WSFS Bank and PwC Philadelphia

- Education: Bachelor’s degree in Accounting from Goldey-Beacom College, Wilmington DE. I’m working towards my MBA in Financial Management, graduating in May 2024.

- Life outside of work: I’m a licensed cosmetologist so outside of work I enjoy styling hair for family and friends. I also like to go on long walks with my chihuahua, Coco.

- Favorite quote: “Independence is doing what you want, knowing that you’re happy with the decisions you’re making and that it’s best for you.” – Jorja Smith

================================================

Stephanie Vance, Administrative Assistant

- Joined Cover & Rossiter: December, 2023

- Prior experience: I worked in several administrative roles, such as, office manager, compliance, and claims manager, for a truck accessory/fabrication shop and Amtrak.

- Life outside of work: I love hanging out with my kids!

- Favorite quote: “Do unto others as you would have them do unto you.” – Golden Rule

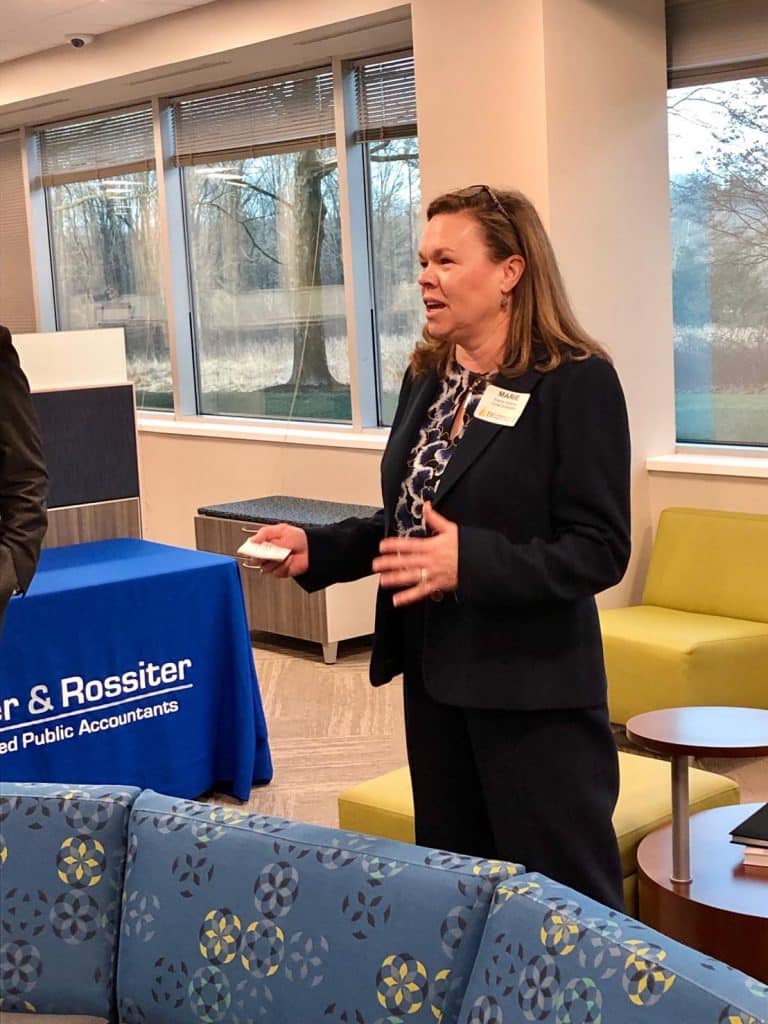

It is with great pride and excitement that we share Marie Holliday, CPA, MBA, our managing director, has been elected as chair of the Delaware State Chamber of Commerce (DSCC)’s Board of Directors—assuming the role following the retirement of Nick Lambrow, Delaware regional president of M&T Bank.

Marie joined Cover & Rossiter in 1997 and was elevated to managing director in 2016. She is a longtime volunteer at the Delaware State Chamber of Commerce having served on multiple committees, including tax and Superstars in Business. In 2019, she joined the DSCC’s Board of Governors and in 2021, she was elected to the Board of Directors to serve as treasurer. She became vice chair in 2022.

“Marie is a natural leader and dedicated advocate for our mission. Her years engaging with our organization as both a member and a volunteer make her an ideal fit as our chair,” said DSCC President Mike Quaranta. “Her leadership will help us grow and thrive as we continue to serve Delaware’s business community.”

“Throughout my tenure at Cover & Rossiter, I’ve had the opportunity to advise clients on such issues as tax compliance, succession planning, growth management consulting, and trust and estate planning. Furthermore, I’ve been privileged to interact with many Delaware business leaders in my various roles with the DSCC and other organizations I support, so I believe I’m ready to take on this role,” shared Holliday. “I plan to continue to support the DSCC’s efforts to advocate on behalf of Delaware businesses in areas such as workforce development training, economic growth, and sustainability. Amazing things can be achieved when we work together to accomplish our goals.”

We know Marie will do a great job advocating on behalf of the DSCC!

Cover & Rossiter, one of Delaware’s first and most respected certified public accounting and advisory firms, is pleased to announce that Samantha Maiorano was one of only 35 CPAs honored by the American Institute of CPAs (AICPA) as a member of the Leadership Academy’s 14th graduating class. Maiorano was selected based on her exceptional leadership skills and professional experience for the four-day Leadership Academy program, held on October 23-27, 2022.

The Leadership Academy was designed to help promising young accounting professionals engage with thought leaders, learn strategies to forge relationships, expand their competencies, and become leaders within the CPA profession. Participants represented all areas of the accounting and finance profession, including public accounting firms, business and industry, government, and consulting firms. The participants were recommended by their employers, state CPA societies and volunteer organizations.

AICPA Chair Anoop Natwar Mehta commented, “It was a privilege to be around such amazing young professionals. They understand the importance of personal development and building relationships. The CPA profession is about people, and AICPA Leadership Academy believes in the importance of developing strong leaders.”

Maiorano is a Supervisor in the Audit Department. Since joining Cover & Rossiter in July of 2016, Sam has focused primarily on non-profits, bringing invaluable knowledge and support to the team. She received her Bachelor’s degree in Accounting at the University of Delaware. Maiorano is a young founder with the Fund for Women, an endowment held at the Delaware Community Foundation that provides grants to support women’s and girls’ programs in Delaware. She is also a mentor for Fresh Start Scholarship. Maiorano enjoys spending her free time with her two daughters.

To date, more than 475 CPAs have participated in the AICPA Leadership Academy, many of whom have gone on to leadership positions within their firms, businesses or volunteer organizations. For more information about the AICPA Leadership Academy, visit: us.aicpa.org/interestareas/youngcpanetwork/cpeandevents/aicpaleadershipacademy

For a full list of graduates, visit: https://insidepublicaccounting.com/2022/11/aicpa-announces-leadership-academy-grads-2/

Cover & Rossiter is an award-winning CPA advisory firm recognized for providing high-quality advice and personalize service to enable their clients to achieve their objectives. The firm is a two-time award winner of the The Marvin S. Gilman Superstars in Business Award presented by the Delaware State Chamber of Commerce.

For more information, contact Lindsay Wheeler lwheeler@coverrossiter.com or 302-691-2224.

Cover & Rossiter, one of Delaware’s first and most respected certified public accounting and advisory firms, is excited to welcome five new members.

Margaret Mendoza joined the Cover & Rossiter team in August 2021 as a staff accountant in the tax department. In May 2021, she graduated from Goldey-Beacom College with a Bachelor’s degree in Accounting, and she is currently pursuing her MBA with a concentration in Financial Management. Before joining C&R, she was the accounts payable specialist for a site management company in Maryland.

Leo Bacchieri began as an intern at Cover & Rossiter in January 2020 while completing his Bachelor’s degree in Accounting at the University of Delaware. Following 6 months of interning, he returned to the University of Delaware to earn his Master’s in Accounting. In August 2021, Leo rejoined Cover & Rossiter as a staff accountant in the tax department. He also has experience as an accounting intern at Santora CPA Group.

Danielle Diaz joined the Cover & Rossiter team July, 2021 as a staff accountant in the tax and audit department. In May 2021, she graduated from Goldey-Beacom College with a Bachelor’s degree in Accounting, and she is currently pursuing her MBA in Finance. She previously participated in an internship in the tax and audit department at Horty & Horty, PA.

Indy Singh joined Cover & Rossiter in November 2021 as a staff accountant after working as an intern during his senior year in college. He earned a Bachelor’s degree in Accounting from Rowan University in May, 2021. In addition, he holds a Bachelor’s in Business Administration from India. Before joining Cover & Rossiter, he was a team leader at GGB in Thorofare, NJ for a CNC Machinist department. Prior to 2017, he was running a business in India providing students consulting service to get enrolled in international universities. He has also worked in the retail sector and construction industry in the UK and New Zealand.

Karen Wright rejoined Cover & Rossiter in October 2021 in the accounting services department as a manager. Her role includes providing top level CFO services to clients as well as working with the client accounting services team to provide such services as software training and consultation, payroll processing, monthly and quarterly review work, budget preparation, and part-time controller services.

Karen graduated from Temple University with a Bachelor’s degree in Accounting. Prior to rejoining Cover & Rossiter, Karen was Finance Director and shareholder for a prominent Delaware engineering firm. She assisted with the renaissance of that firm, which made it highly profitable and led to a lucrative merger. Karen has also provided accounting services to multiple small businesses along the way, including her husband’s IT consulting business.

Cover & Rossiter is one of the first and most respected full-service CPA & advisory firms in Delaware, providing tax, audit, trust, and accounting services to individuals and families, businesses, nonprofits, and captive insurance companies. The firm is a two-time winner of The Marvin S. Gilman Superstars in Business Award presented by the Delaware State Chamber of Commerce.

For more information, contact Lindsay Wheeler, lwheeler@coverrossiter.com, 302-691-2224.

Cover & Rossiter, one of Delaware’s first and most respected certified public accounting and advisory firms, is pleased to announce the following promotions.

Peter Hopkins has been promoted to Principal in the Tax Department. Hopkins joined Cover & Rossiter in 2015 and has established a reputation for his excellent analytical skills, broad technical knowledge and commitment to optimizing his clients’ tax situation. In his words, “I work with clients to plan for and minimize their taxes; for those who prefer not to plan, I do damage control.” Previously, he spent 20 years practicing public accounting in New York City.

In between New York City and Delaware, Hopkins lived in Indonesia for four years and can speak Indonesian conversationally. He is certified in Teaching English as a Foreign Language and Teaching Business English. During his free time, Hopkins enjoys traveling and spending time with his wife and daughter as well as cooking, reading nonfiction, and following sports.

Hopkins is a member of the American Institute of Certified Public Accountants. He received his Bachelor’s degree in Business Administration in Public Accountancy and his Master of Science in Taxation from Baruch College. Hopkins is also an Eagle Scout with the Boy Scouts of America and has served as a volunteer Scout leader for many years.

Samantha Maiorano has been promoted to Supervisor in the Audit Department. Maiorano joined Cover & Rossiter in July 2016. She received her Bachelor’s degree in Accounting at the University of Delaware. Maiorano is a young founder with the Fund for Women, an endowment held at the Delaware Community Foundation that provides grants to support women’s and girls’ programs in Delaware. She is also a mentor for Fresh Start Scholarship. Maiorano enjoys spending her free time with her two daughters.

Rebecca Furey has been promoted to Senior Accountant. Furey joined Cover & Rossiter full-time in September 2020. She earned her Bachelor’s degree in Accounting from Widener University. While completing her degree, she held two internships at Cover & Rossiter in the Tax Department in 2019 and 2020.

Cover & Rossiter is one of the first and most respected full-service CPA & advisory firms in Delaware, providing tax, audit, trust, and accounting services to individuals and families, businesses, nonprofits, and captive insurance companies. The firm is a two-time winner of The Marvin S. Gilman Superstars in Business Award presented by the Delaware State Chamber of Commerce.

For more information, contact Lindsay Wheeler, lwheeler@coverrossiter.com, 302-691-2224.

Cover & Rossiter, one of Delaware’s first and most respected certified public accounting and advisory firms, is pleased to announce that Pete Kennedy has been invited to join the board of the Delaware Community Foundation (DCF).

Kennedy, a director at the firm, joined Cover & Rossiter in 1999. As head of the Audit practice, he has expertise in nonprofit accounting, auditing, and tax issues, and is privileged to work with many of the region’s leading not-for-profit institutions.

DCF President and CEO, Stuart Comstock-Gay, said “Pete has been a volunteer and friend to the DCF for years, and we are delighted to welcome him to our board. His incredible expertise in all areas of nonprofit accounting is sure to be tremendously valuable as we continue our mission of growing philanthropy in Delaware.”

In addition to his new role on the board, Pete is a member of the State of Delaware Plans Management Board, the Board Treasurer for Delaware College Scholars, and a member of the EastSide Charter School Citizens’ Budget Oversight Committee.

“It is a wonderful tribute to Pete to be asked to join the DCF board,” said Marie Holliday, Managing Director of Cover & Rossiter. “He has been a long-term adviser to them, and to be asked to join this leading nonprofit board is so exciting for Pete and Cover & Rossiter.”

Cover & Rossiter is one of the first and most respected full-service CPA & advisory firms in Delaware, providing tax, audit, trust, and accounting services to individuals and families, businesses, nonprofits, and captive insurance companies. The firm is a two-time winner of The Marvin S. Gilman Superstars in Business Award presented by the Delaware State Chamber of Commerce.

For more information, contact Lindsay Wheeler, lwheeler@coverrossiter.com, 302-691-2224.

It is with great honor that Cover & Rossiter’s Managing Director, Marie Holliday, has accepted the responsibilities of being the vice chair and treasurer of the Delaware State Chamber of Commerce Board of Governors. In 2021, Holliday was recognized by the Delaware State Chamber of Commerce as its Board Member of the Year. The DSCC staff chose Holliday as the honoree for her leadership, guidance, and volunteer time towards the Superstars in Business awards program.

Holliday has agreed to serve as chair of the chamber’s board in 2022 following Nick Lambrow’s term. Holliday said, “I have enjoyed learning from Katie Wilkinson, outgoing board chair, and Nick as they have led the chamber. They have helped me feel prepared for this exciting challenge.”

Cover & Rossiter has been a long-term member of the chamber and been recognized multiple times by the chamber with the Marvin S. Gilman Superstars in Business (Superstars in Business winner 2018 and 2012; Award of Excellence Winner 2017 and 2011).

Holliday joined Cover & Rossiter in 1997 and quickly applied her extensive experience in tax research and corporate tax planning to assist numerous clients in addressing a wide variety of tax situations. She has always been focused on finding tax-advantaged solutions for clients to influence future growth and sustainability. Holliday’s client base includes medical professionals as well as medical practices. Most recently, she assisted clients with maximizing the opportunities made available to them as a result of the COVID pandemic. This included assistance with PPP applications, loan forgiveness applications, Employee Retention Tax Credits and other similar assistance programs.

Holliday has been Managing Director of Cover & Rossiter since 2016. She is responsible for the strategic direction of the firm as well as leading the firm’s tax and advisory services departments. She has guided the firm’s expansion and growth in business segments such as captive insurance, trusts, and Growth Management Consulting, the firm’s one-stop solution for developing sustainable growth strategies that help clients address the full range of challenges they face every day.

Holliday serves on the Board of Governors of the Delaware State Chamber of Commerce and the Professional and Personal Liability Insurance Program Committee for the American Institute of Certified Public Accountants (AICPA). She is also a member of the Delaware Banker’s Association, Delaware Society of CPAs, Estate Planning Council of Delaware, and Wilmington Tax Group. She is a sought-after speaker or panelist on the ever-changing tax laws, having presented to audiences at Delaware Technical Community College, Medical Society of Delaware, and the Delaware Trust Conference, to name a few.

We are thrilled to announce that Andy Johnson, Principal at Cover and Rossiter, has completed the ConvergenceCoaching® Spring Transformational Leadership Program™.

Andy has been an employee in the tax department since 2008. His primary focus is helping clients navigate the constantly changing tax landscape. In addition, he has taken on a leadership role in evaluating and implementing new technologies intended to help shape Cover & Rossiter as a CPA and advisory firm positioned for growth well into the future. With his exceptional problem-solving skills and attention to detail, Andy is an incredible asset to the C&R team.

“I am continuously impressed by Andy’s relationships with clients, work ethic and determination to enhance his leadership skills. The firm, and our clients in particular, will continue to benefit from Andy’s tax expertise and guidance!”

Marie Holliday, Managing Director at Cover & Rossiter

ConvergenceCoaching®, LLC, is a national leadership and management consulting firm that helps public accounting and consulting firms achieve success. Their Transformational Leadership Program (TLP) is a one-year accelerated “finishing school” for CPA and consulting firm new partners and emerging leaders. The TLP focuses first on individual mindset and behavior to drive change in thinking and personal responsibility, followed by strategies and actions to prepare them to lead their firm into the future. This program consists of assignments, workshops, coaching, and more, and allows leaders to evolve and challenge themselves to best support their clients and their company.

Congratulations Andy!